Energy Update

Quick dissection of power status quo and government’s direction

-

Urja Khabar

Urja Khabar

- 26 July, 2023

Kathmandu; With nearly 2,666 MW of hydel projects Nepal has negligible seasonal pondage projects. Due to the limited generation capacity during the dry season, it is always a challenge for the Nepal Electricity Authority (NEA) to meet the peak demand of nearly 2,200 MW.

As per NEA report of F/Y 2021/22, the domestic consumer connection covers 92.71% (comprising the sales of 42.1%), industrial consumers 1.36% (comprising the sales of 38.98%), and others 5.93% (comprising the sales of 18.91%). The low industrial consumers might be either due to the adverse energy assurance, or the overall geo-political situation is less conducive for the industries. Not to forget, the current demand is just the suppressed one. What would be the maximum demand during the peak hours, if the industrial load will represent in the range of 70-90% of the total demand? However, it is beyond our imagination of load shifting towards industrial consumption, at least in the current context. None of the available industries in Nepal can imagine their productions without backups, especially of diesel generators.

This is due to the unreliability of the grid supply. Also, they are not fed with enough supply; case of dedicated feeder to the high energy demanding industries. If that would have been the case, the production cost would have been reasonably low to compete with the import of goods from neighbouring countries.

As per the Nepal Energy Sector Synopsis Report -2022, traditional fuel consumption covers nearly 66.3%, renewables & electricity 6.6%, and the commercial energy consumption aggregate to 27.1%. The energy consumption by fuel types clearly indicates the shift of Nepalese energy consumption pattern by fuel types from traditional sources to commercial; renewables are almost in the stagnant stage. This shift of traditional fuel consumption towards commercials is not a sustainable approach since we have no such commercial fuel resources. This will ultimately upsurge the import of commercial fuels leading to ever-widening trade gap.

Nepal with tremendous hydroelectricity potential also lies in a solar belt with abundant radiation with nearly more than 300 sunshine days a year or little more. Both are sustainable sources of energy. However, we are in a state of energy deficiency. SDG has set the target for the energy mix which states, “By 2030, increase substantially the share of renewable energy in the global energy mix”.

The necessity of energy mix as portrayed by SDG is being internalized in Nepal as well. To execute the same, NEA has a policy for Power Purchase Agreement (PPA) with private developers of solar energy for at least 500 W or above. However, the PPA rate is contextualized to be Rs 5.94 (down from Rs 7.30) from mid-July 2022, which will further be bid for a competent rate, meaning below the rate of Rs. 5.94. In line with the contextualized PPA rate, one of the many arguments could be NEA procrastinating the PPAs. NEA is wooing for electricity export.

Even the assumed ‘breakthrough’ of cross-border trade with India and Bangladesh in recent visit of Pushpa Kamal Dahal is yet in the womb of the future. India stands first place in commitments but procrastinates in executions. However, the current situation of India looking for financial closures of each hydropower projects is no more than merely a full of prejudice and meddling decisions.

Let keep up watching as the situations keeps unfolding. Diminishing consumption of traditional fuels which being compensated by a surge in the commercial ones merely increasing trade deficit in the name of cleaner fuel. Renewable energy sources are progressing in an encouraging pattern but due to the lowest share, it is so minuscule that changes are less visible.

A concrete study comparing the necessity of pipeline construction, increasing gasoline storage capacity vs massive upgradation of distribution lines and some transmission lines is deemed necessary. The integrated planning approach is often overlooked in underdeveloped and developing countries. It is evident that the gasoline storage capacity of NOC is far below the international threshold. However, before taking an arbitrary leap, it should be scientifically justified; is it the right time to increase the storage capacity? Is it the right time to develop pipelines for gasoline? What if we transfer the gasoline investments for pipeline and storage capacity to enhancing the electricity distribution network and contribute to replacing the fossil fuel consumption?

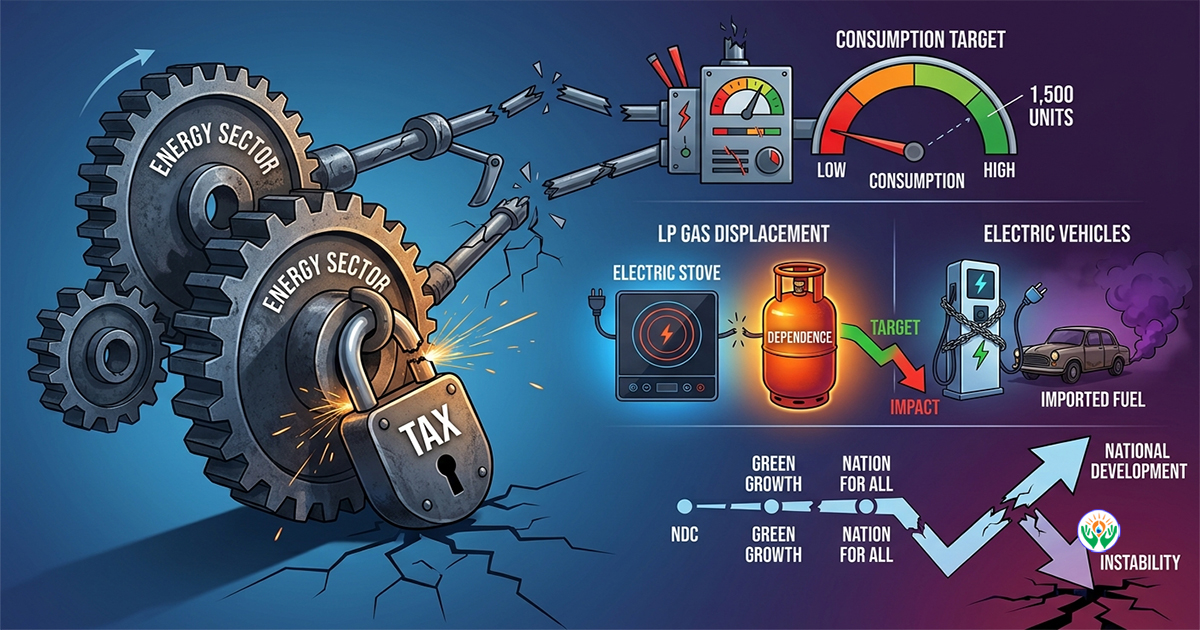

National targets to increase electricity per capita by the increase in adoption of electric cook stoves and EVs are astonishing against its activities by increasing tax on electric vehicles, subsidy in LPG, and increasing the storage capacity of gasoline fuels. What an irony! What about the NDC target to decarbonize the transportation sector? NDC target spells “sales of electric vehicles in 2025 will be 25% of all private passenger vehicles sales, including two-wheelers and 20% of all four-wheeler public passenger vehicles sales in 2025”.

However, the fiscal budget of 2023/24 does not look intended to support EVs promotion, except some minor corrections, overall the taxations are on uptrend. Similarly, in the cooking sector, NDC spells “ensure 25% of households use electric stoves as their primary mode of cooking by 2030”. However, public in unaware of implementing strategies to achieve these targets, which are not even clearly portrayed in the current fiscal budget.

Need to re-think, if there are any latent approaches to achieve the net-zero target by extending the gasoline pipelines and increasing gasoline storage capacity.

Pondering - WHY?

Is there enough research regarding the benefits of gasoline storage capacity and pipeline vs enhancing the distribution line and the pondage projects? Why has the policy dialogue with India so far seems less impactful? Do we have research-based and tailor-made approaches and diplomacy to sell green electricity to India? If yes, why does India seem reluctant to buy such needy green electricity to meet their SDG target on decarbonization?

Why are we not able to sell such nutritious and alluring food to someone who is hungry with pockets full of dollars? Why are we even making the sales of such a superfood at the stage when we ourselves are malnourished? Just because we don’t have proper plates to serve?

The electricity export issue should not be the first point for discussion rather electricity distribution line enhancement should be. Business as usual movement is not acceptable. Speed up. The priority should be focused on in-house consumption and that is only possible with massive upgradation of distribution networks. We need a concrete policy and plan to increase both the domestic and industrial load. What will be the consequences, if 25% of 6 million households, as per the NDC target, would adopt electric cooking? What if GoN designs and implements vehicle conversion plants (old fossil fuel vehicles to EVs) backed up with charging stations? Massive industrial consumption of electricity can be pivotal for the shrinking Nepalese economy and chase some aspiring economic growth.

Let’s re-think if it is high time to do our homework more scientifically; evidence-based. If GoN needs a dedicated wing or think-tank, issue-based-wing, to pursue real time scientific research for integrated energy planning in-house and for the cross-border trade.

Dr. Sanjel holds a Ph.D. in Energy Planning and is an energy professional for last one and half decade.

Conversation

More News

- Nepal's First Energy Based News Portal

-

Energy Information Center Pvt. Ltd.

Hemant Marg-11, Babar Mahal, Kathmandu

- Info. Dept. Reg. No. : 254/073/74

- Telephone : +977-1-5321303

- Email : [email protected]